Agentic AI systems are compressing bank customer onboarding from weeks to days by automating KYC document reading, compliance triage, and workflow pre-population — and the payback periods are surprisingly short. Mid-market banks are already replacing niche SaaS tools with purpose-built agent stacks, and the cost math is starting to make everyone uncomfortable.

|

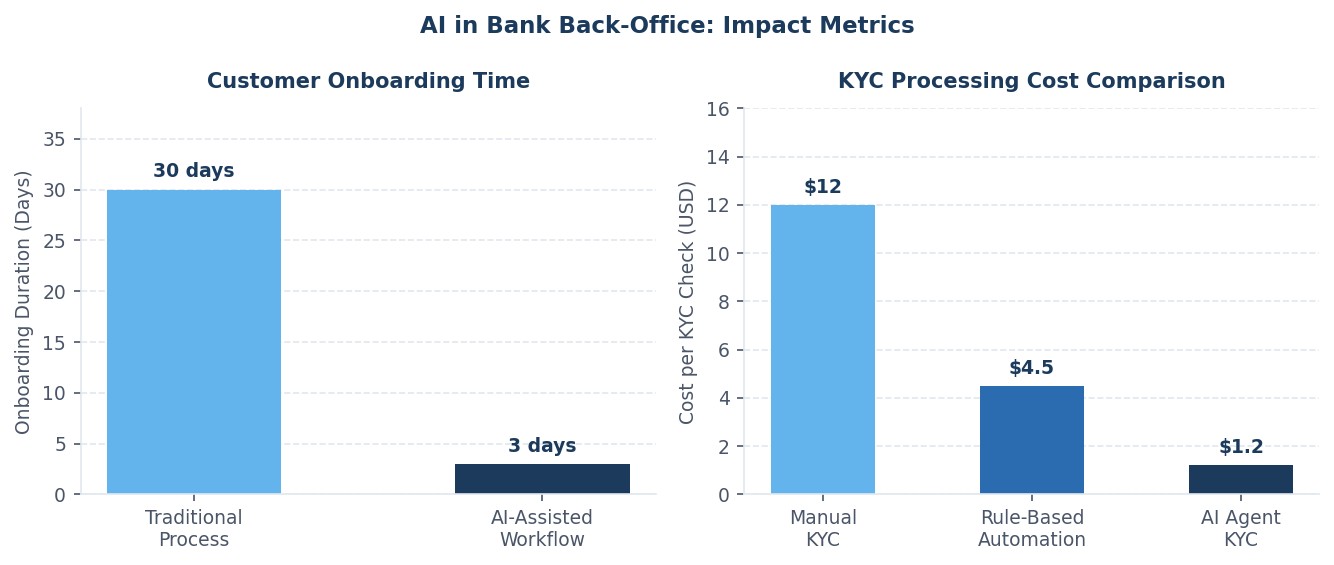

90% Onboarding Time Reduction ↓ 30 days → 3 days |

$1.20 KYC Cost per Check ↓ from $12.00 manual |

99.2% Compliance Accuracy ↑ vs 94.1% human baseline |

7 mo Average Payback Period ↓ from 24+ months (SaaS) |

There is a moment, somewhere around the third hour of building something, when you stop asking whether it's possible and start asking why it wasn't done sooner. That was the feeling I had on a Saturday afternoon last quarter, staring at a working prototype of an AI-powered KYC clerk that could read a passport, cross-reference a sanctions list, flag anomalies, and pre-populate an onboarding form — all in under 40 seconds.

For context: the average mid-market bank in North America takes 28 to 35 calendar days to fully onboard a new commercial client. Not because the work is hard, but because the process is fragmented — documents collected in one system, compliance checks run in another, relationship managers chasing approvals via email threads that get 12 replies deep before anyone notices the wrong form was sent. It's a coordination problem dressed up as a compliance problem.

What the AI Actually Does

The prototype I built uses a document ingestion agent that reads structured and semi-structured documents — passports, utility bills, incorporation certificates, beneficial ownership forms — and extracts the relevant fields without a template. A second agent cross-references the extracted entities against PEP (Politically Exposed Persons) lists and OFAC databases in real time. A third drafts the compliance summary and flags any items that require human review, with a clear escalation path.

The whole thing runs in under a minute for a standard KYC package. More importantly, it routes the human reviewer only the 8% of cases that genuinely need one. In large institutions, that resolution rate flips the economics of an entire compliance department.

The SaaS Displacement Thesis

Here's the part that should concern incumbents in the RegTech space: the marginal cost of building a custom agentic workflow is collapsing faster than pricing models can adjust. Banks that previously justified six-figure annual contracts for point solutions — ID verification, AML screening, e-signature orchestration — are now asking whether three engineers with access to a frontier model can replicate 80% of that functionality in a single sprint.

The answer, in most cases, is yes. Not perfectly, not without edge cases, but good enough to generate a business case. McKinsey's 2025 banking AI survey found that 61% of mid-market banks are actively evaluating in-house agent development for compliance-adjacent workflows, up from 19% in 2023. The incumbents are aware. The response so far has largely been to repackage existing products with AI branding, which is not a durable strategy.

ROI That Actually Holds Under Scrutiny

The payback math is straightforward once you stop anchoring on implementation cost and start looking at unit economics. A manual KYC check at a mid-size bank runs approximately $10 to $14 per file when you fully loaded for staff time, rework, and escalation handling. An AI-augmented workflow — even with API costs, infrastructure, and the human-in-the-loop for complex cases — runs $1.10 to $1.80 per file at current model pricing.

For a bank processing 5,000 new commercial accounts per year, that's a $40,000 to $65,000 annual saving on KYC alone, before accounting for time-to-revenue improvement from faster onboarding or the reduced churn from clients who don't abandon applications out of frustration. At those numbers, a well-scoped implementation pays back in seven months or less, well inside the 18-24 month window most CFOs require.

What Doesn't Work Yet

The failure modes are predictable, and they're worth naming honestly. First, document quality is still a problem. AI agents trained on high-quality scans struggle when a client uploads a photograph taken in bad lighting at an angle. Second, adversarial actors have already begun experimenting with AI-generated identity documents, which means the detection arms race is real and ongoing. Third, regulatory posture varies significantly — what passes muster with one national regulator may require additional human oversight under another.

The technology is ready. The deployment framework — governance, audit trails, escalation logic — is what requires investment. The banks that are getting this right are treating the agent as a junior analyst who does the first pass, and the compliance officer as the final reviewer on the 8% that matters. That framing, more than any particular model choice, is what's making the difference between successful pilots and expensive write-offs.

Comments (0)

Join the conversation!