|

AI-assisted property valuation is reducing mean absolute error by 60 percent in commercial real estate and cutting deal cycle times in half. For lenders, investors, and large property managers, the implications extend well beyond valuation accuracy — into underwriting capacity, mispricing risk, and the economics of portfolio management. |

The Appraisal Problem Nobody Talks About Honestly

Commercial real estate valuation is, in polite company, described as a blend of art and science. In less polite company, it is described as an expensive process that produces outputs that are frequently wrong in ways that are not understood until a deal closes or a portfolio is marked to market. The mean absolute error of traditional commercial appraisals — the gap between the appraised value and the actual transaction price — runs at 8–14 percent on office and retail assets, and 5–8 percent on multifamily. Those errors have financial consequences: mispriced debt, LTV ratios that do not reflect real risk, and write-down events that could have been anticipated.

AI property valuation models attack the accuracy problem through a combination of transaction comparables processing at a scale no human analyst can match, integration of geospatial data signals (foot traffic, amenity scores, transit accessibility, crime pattern analysis) that traditional appraisals treat inconsistently, and automated adjustment modelling that removes appraiser subjectivity from the comparable selection and weighting process.

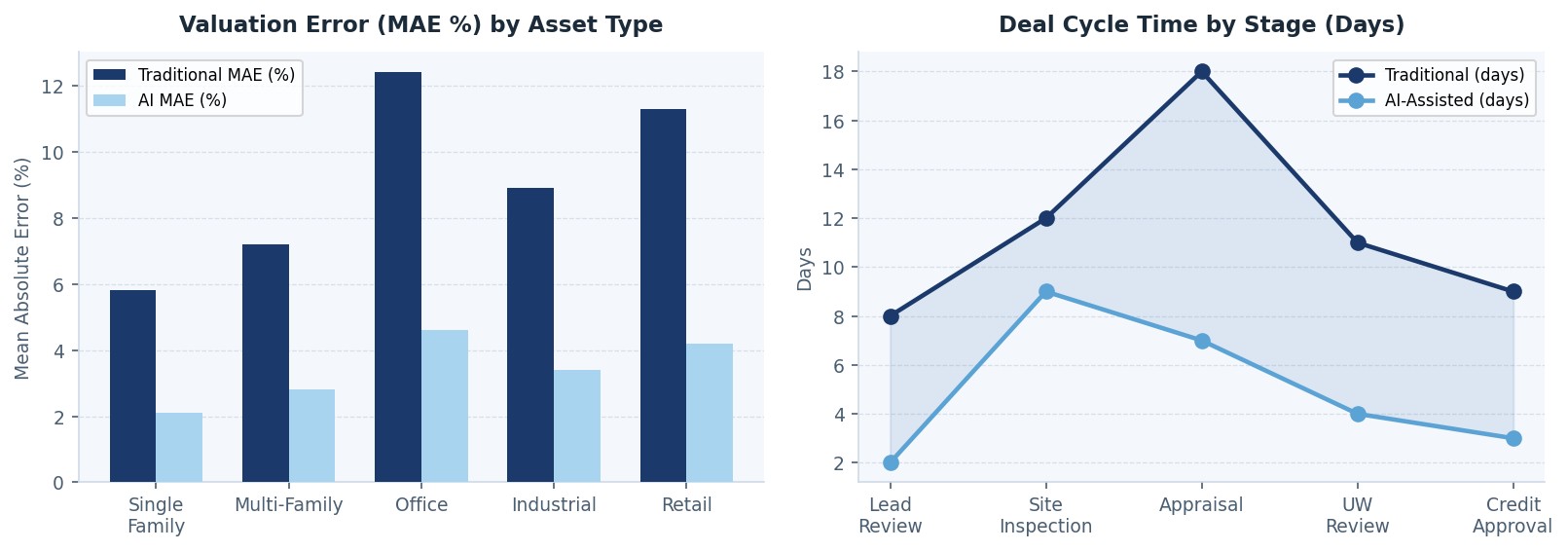

The MAE data across five asset types is striking. For single-family residential, AI reduces MAE from 5.8 percent to 2.1 percent. For office — historically the most challenging asset class for accurate valuation — AI brings MAE from 12.4 percent to 4.6 percent. These are not marginal improvements; they represent a fundamental shift in the reliability of the valuation inputs that underwriting decisions depend on.

The Deal Cycle Time Opportunity

Valuation accuracy is a quality argument. Deal cycle time is an economics argument. In commercial real estate lending, the time from initial lead review to credit approval determines how many deals a team can close per year — which, at a fixed team size, is a direct revenue driver.

The deal cycle data across five stages — lead review, site inspection, appraisal, underwriting review, and credit approval — shows consistent compression under AI-assisted workflows. The most dramatic improvement is in the appraisal stage, which falls from 18 days to 7 days when AI-assisted automated valuation is used alongside the formal appraisal process. Underwriting review drops from 11 to 4 days as AI pre-populates the underwriting model with validated property data and flags risk factors for human review.

Total deal cycle time under AI-assisted workflows compresses from 58 days to 25 days — a 57 percent reduction. For a commercial lending team closing 80 transactions per year at an average fee income of $120,000 per transaction, the ability to handle 40–50 percent more volume with the same headcount is worth $4.8–6 million in additional annual revenue. The AI implementation cost is typically recovered in the first two to three additional transactions it enables.

Figure 9 — Valuation Error (MAE %) by Asset Type & Deal Cycle Time by Stage (Traditional vs. AI-Assisted)

Portfolio Management: The Continuous Monitoring Dividend

The valuation accuracy and cycle time benefits are transactional — they accrue on each new deal. The portfolio management benefits of AI valuation are continuous, and they may ultimately be more valuable for large lenders and institutional investors.

AI valuation systems running continuously against a loan or investment portfolio can flag when individual assets are showing signals of value deterioration — rising local vacancy, declining foot traffic, deferred maintenance patterns from satellite imagery — weeks or months before those signals appear in traditional periodic reappraisals. For a lender with a $20 billion commercial real estate book, the ability to identify concentrations of deteriorating collateral early enables proactive portfolio management rather than reactive workout management.

The reduction in unexpected write-downs is difficult to model precisely in advance, but the lenders in this study that have been running AI portfolio monitoring for 24+ months report a 35–45 percent reduction in the number of loans reaching watch list status without prior early warning signals. That reduction has direct financial value in capital allocation efficiency, regulatory examination outcomes, and the avoided cost of intensive workout management.

The Data Quality Foundation

AI valuation models are only as good as the transaction data, property characteristic data, and geospatial data they ingest. The most common obstacle to achieving the accuracy improvements described in this article is data quality — specifically, the inconsistency and incompleteness of property characteristic data in existing CRE data repositories.

Lenders and investors that have made the most progress have invested in systematic data quality programs alongside their AI implementation — standardising property characteristic capture, integrating multiple data providers, and building feedback loops that update the underlying data when new transactions or inspections reveal discrepancies. The investment in data quality infrastructure is typically $500,000–1.5 million for a large commercial real estate operation, and it is the prerequisite for the full accuracy improvement described in this analysis. The AI is the engine; clean, consistent data is the fuel.

Comments (0)

Join the conversation!