Professional services firms built on hourly billing are facing an existential tension: the AI tools that make their people 3x more productive are also compressing the number of hours clients are willing to pay for. The firms navigating this successfully aren't resisting the change — they're repricing their value proposition entirely.

|

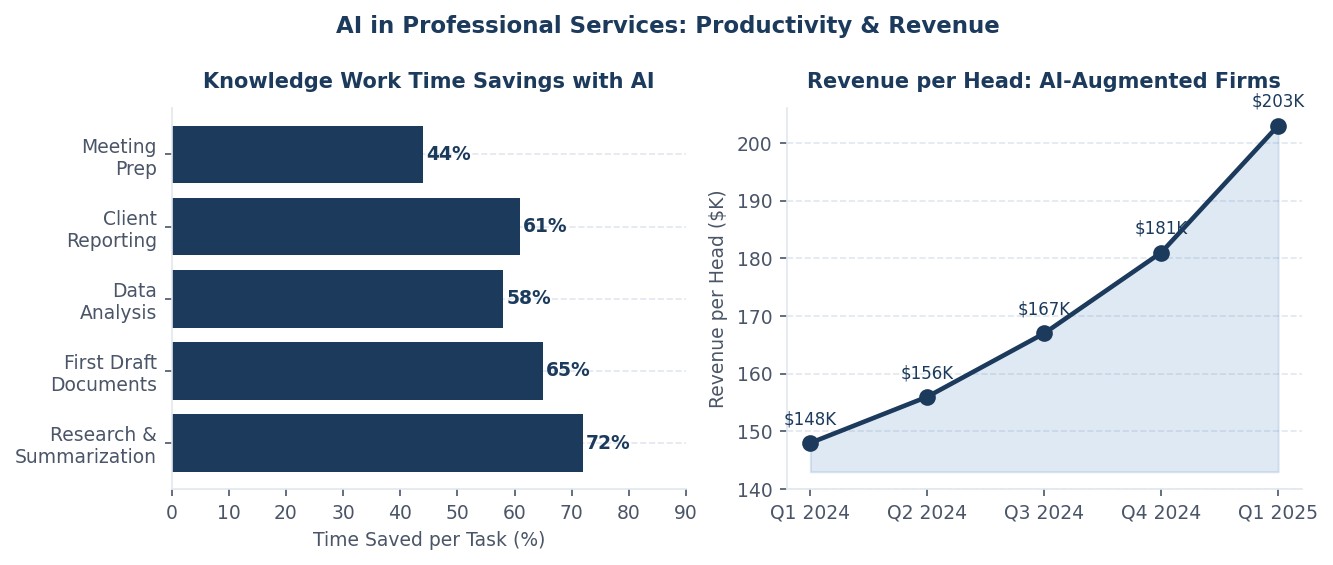

61% Knowledge Work Time Saved ↑ on research & first drafts |

$203K Revenue per Billable Head ↑ 37% since Q1 2024 (AI-native) |

94% Client Retention Rate ↑ AI-augmented firms vs 81% trad. |

+22pt Proposal Win Rate ↑ AI-assisted bid teams |

A senior partner at a mid-size strategy consulting firm told me something that stuck with me: "The first time I watched a junior analyst produce a first draft that used to take two days in forty minutes, I didn't feel excited. I felt sick." That reaction is more common than the industry publicly admits. Because what he was watching was not just a productivity gain — it was a repricing event for a service his firm had been selling at a particular premium for thirty years.

Professional services — consulting, legal, accounting, financial advisory, architecture, market research — are facing a structural tension that no amount of AI strategy framing can fully dissolve. The billable hour model prices time. AI reduces time. The math is uncomfortable.

What's Actually Getting Automated

The honest answer is: a lot. Research synthesis — the process of reading hundreds of documents, extracting relevant information, and presenting a structured overview — is almost entirely automatable at a quality level that passes partner review with minor edits. First-draft document generation for standard deliverable types — market analysis, competitive benchmarks, due diligence summaries, contract first drafts — is similarly compressible. Meeting preparation, data cleaning, financial model population, regulatory filing preparation: these are all being compressed by 50-75% in firms that have made the tooling investment.

What's not being automated is judgment — the ability to synthesize ambiguous information into a defensible recommendation, to read a room during a difficult client conversation, to know which questions to ask before the client knows what they need answered. The value of that judgment, however, is now decoupled from the time cost of producing the supporting analysis. That decoupling is where the billing model breaks down.

The Firms Adapting Fastest

The professional services firms growing fastest right now share a few characteristics. They've moved toward outcome-based pricing for an expanding share of their work — fixed fees for defined deliverables, success fees tied to client outcomes, retainer structures that compensate for access to judgment rather than hours of junior analyst time. They've dramatically reduced the ratio of junior to senior staff, investing the efficiency dividend in fewer, higher-caliber people. And they've made AI proficiency a first-class hiring criterion rather than a nice-to-have.

A boutique strategy firm in the 50-person range that has rebuilt its delivery model around AI-augmented workflows is reporting revenue per head of $190,000 to $220,000 — meaningfully above the industry median of $140,000 to $160,000. The premium reflects not just efficiency but the ability to take on more complex, higher-stakes work that requires senior judgment applied rapidly.

The Firms at Most Risk

The firms at greatest risk are those that have built their margins primarily on high-volume, process-heavy work delivered by large junior staff pyramids — document review, data gathering, compliance checking, research support. These are exactly the task categories where AI delivers 60-80% time compression. The economic pressure here is severe and accelerating.

The window for structural adaptation is narrowing. Clients are beginning to ask, explicitly, whether AI is being used in delivery — and to adjust their willingness to pay for time-intensive work accordingly. Firms that can answer that question credibly and demonstrate outcomes-based value propositions are building competitive moats. Firms that cannot are being repriced.

Comments (0)

Join the conversation!