AI-driven credit models are reshaping who gets approved and who gets left behind. The efficiency gains are real, but so are the human stories at the margins.

Marcus had done everything right. Twenty-two years at the same employer, a credit score north of 740, and a down payment that represented a decade of disciplined saving. When his mortgage application came back denied, the loan officer looked almost as confused as he did. The culprit was not a missed payment or an unstable income. It was an algorithmic risk model that had flagged a pattern in his financial history—frequent small transfers between accounts—as anomalous behavior. No human had reviewed the decision before the letter arrived.

The Efficiency Dividend

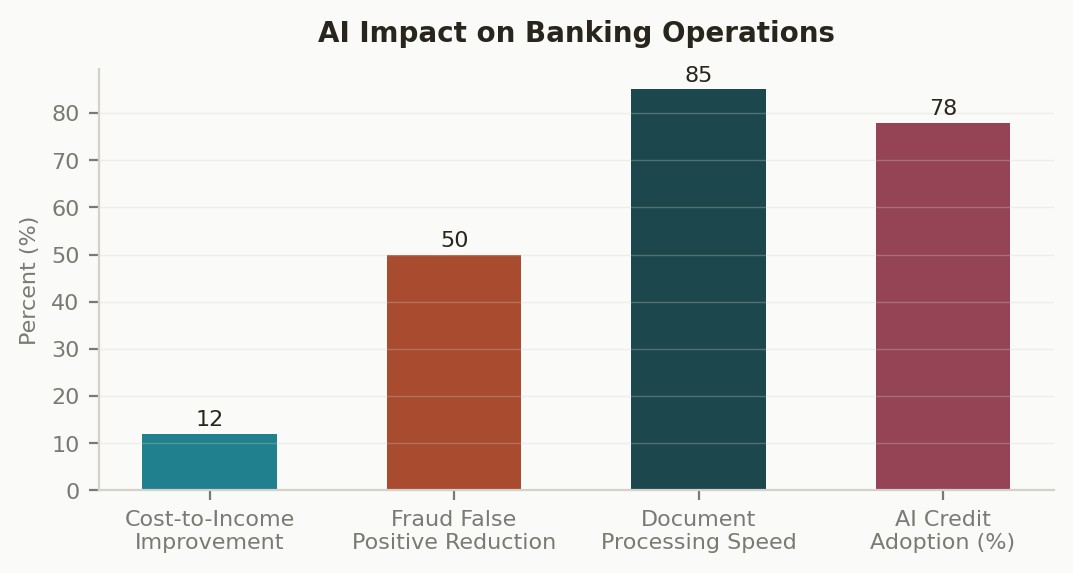

There is no question that AI-powered credit risk systems are transforming banking economics. According to McKinsey’s 2025 Global Banking Annual Review, banks that have deployed AI across credit decisioning, fraud detection, and document processing are seeing cost-to-income ratios improve by 5 to 15 percentage points. JPMorgan alone processes more than $150 million worth of commercial loan documents annually through AI systems, cutting turnaround times from weeks to hours. Oliver Wyman’s analysis estimates that AI-based fraud detection models have reduced false-positive rates by 40 to 60 percent at leading institutions, saving billions in operational overhead.

These are not marginal improvements. They represent a structural shift in how banks operate, price risk, and allocate capital. KPMG’s 2025 survey of financial services executives found that 78 percent of large banks now use AI in at least one core credit function, up from 45 percent just three years prior.

Who Gets Caught at the Edges

But efficiency at scale does not mean fairness at the individual level. The same models that reduce aggregate default rates can encode historical biases or flag legitimate behavior as suspicious. The Bank for International Settlements warned in its 2024 fintech stability report that AI credit models trained on historical lending data risk perpetuating discriminatory patterns—particularly against borrowers in communities that were systematically underserved long before algorithms entered the picture.

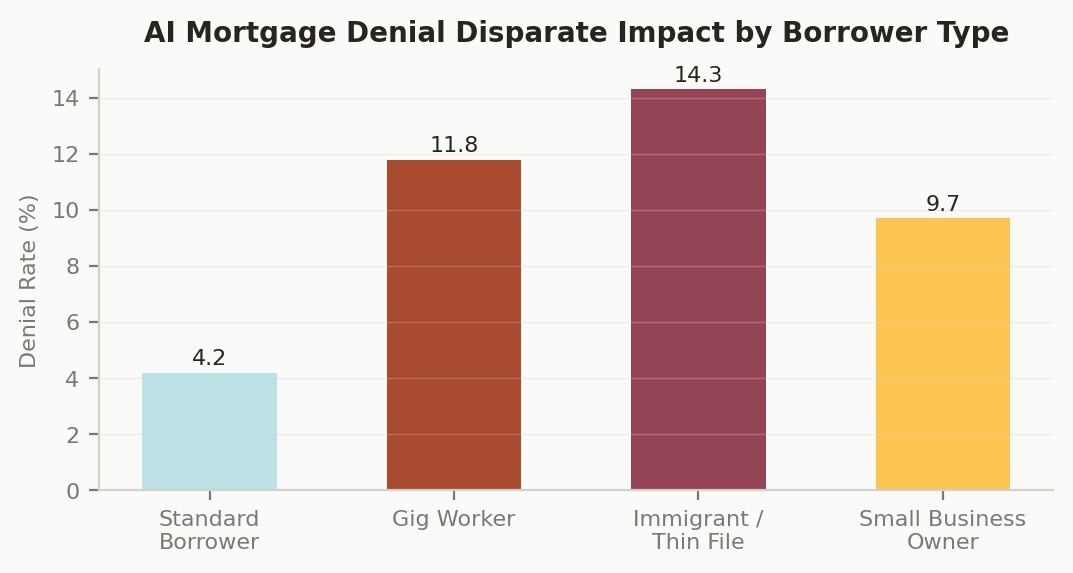

Marcus’s case is not unusual. Consumer financial protection data suggests that AI-driven mortgage denials disproportionately affect borrowers whose financial patterns do not match the model’s definition of “normal”—gig workers with variable income, immigrants with thin credit files, and small business owners who move money frequently between personal and business accounts. The model does not intend to discriminate. It simply optimizes for patterns that correlate with repayment, and those patterns carry the fingerprints of a financial system that was never neutral to begin with.

The Accountability Gap

What compounds the human cost is the opacity of the decision. When a human underwriter denies a mortgage, there is a conversation—a reason you can challenge, a judgment you can appeal to. When an algorithm does it, the denial often arrives as a fait accompli. KPMG reports that only 34 percent of banks with AI credit systems have implemented meaningful explainability frameworks for customer-facing decisions. The rest rely on generic adverse-action notices that tell borrowers almost nothing about why they were flagged.

This is not just a customer experience problem. It is a trust problem that threatens the social contract between banks and the communities they serve. And it is a regulatory problem: the Bank for International Settlements and the European Banking Authority have both signaled that unexplainable AI decisions in consumer lending may not survive the next wave of compliance requirements.

What This Means for You

If you are a borrower:

• Request a detailed explanation of any AI-influenced denial. Regulators increasingly require that lenders provide one. If the answer is vague, escalate to the institution’s compliance office or file a complaint with your national consumer protection authority.

If you are a bank executive:

• Invest in explainability now, before regulators mandate it on less favorable terms. Implement human review for any AI denial that falls outside clear-cut risk thresholds. The cost of a second look is trivial compared to the cost of a discrimination lawsuit.

If you are a front-line banker:

• You are the human face of a system that increasingly makes decisions without you. Advocate internally for tools that let you understand and explain AI decisions to customers. Your credibility—and your institution’s—depends on it.

REFERENCES

1. McKinsey & Company, "Global Banking Annual Review 2025" — https://www.mckinsey.com/industries/financial-services/our-insights

2. Oliver Wyman, "AI in Financial Services: Fraud Detection Benchmarks" — https://www.oliverwyman.com/our-expertise/industries/financial-services.html

3. JPMorgan Chase, "Institute Research: AI Deployments" — https://www.jpmorganchase.com/institute

4. Bank for International Settlements, "Fintech and Financial Stability" — https://www.bis.org/topic/fintech.htm

5. KPMG, "AI in Financial Services 2025" — https://kpmg.com/us/en/articles/2024/ai-in-financial-services.html

Comments (0)

Join the conversation!