Automated valuation models have existed for decades, but the combination of satellite imagery, alternative data sources, and large-scale machine learning is producing property pricing signals that increasingly outperform traditional appraisals — and creating competitive advantages for the investors and brokerages that use them first.

|

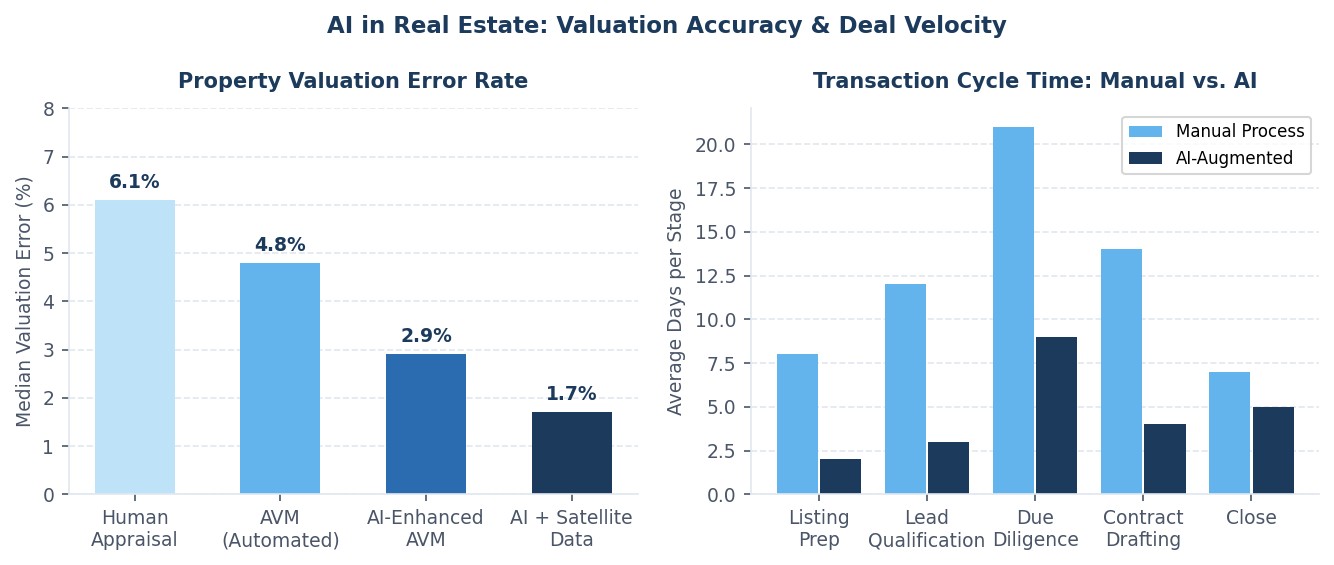

1.7% AI Valuation Error Rate ↓ vs 6.1% traditional appraisal |

↓ 55% Deal Cycle Reduction AI-augmented transaction teams |

+340% Off-Market Deal Discovery ↑ AI-driven lead identification |

↑ 4x Portfolio Risk Flag Rate Earlier identification vs manual |

The way property gets priced has barely changed in a century. An appraiser walks through the property, notes its condition, identifies three comparable sales in the vicinity, and adjusts for the differences — square footage, renovation quality, view, proximity to amenities. It's a skill-intensive, time-consuming, largely subjective process that produces an opinion of value with meaningful uncertainty bands, typically plus or minus 5-8% in stable markets.

AI valuation models are doing something qualitatively different. They're not looking for three comparables — they're ingesting thousands. They're pulling assessor records, permit histories, HOA financials, flood zone data, school rating trajectories, crime statistics, walkability scores, and, increasingly, satellite and street-level imagery that proxies for property condition without requiring a physical visit. The result is a pricing signal that is faster, more consistent, and in well-data-covered markets, more accurate than the traditional appraisal process.

The Alternative Data Advantage

The most interesting applications of AI in real estate aren't the public-facing consumer tools like Zillow's Zestimate — they're the institutional investment tools that most retail participants don't see. Quantitative real estate funds are running satellite imagery analysis to detect construction permit activity before it appears in public records, identifying neighborhoods in early-stage gentrification patterns through parking lot fill rates, retail turnover, and permit density. They're correlating social media restaurant openings and closings with micro-neighborhood price trajectories.

These signals have predictive power. A model trained on satellite-derived construction activity in a metro area can identify emerging demand hotspots six to twelve months before the price movement shows up in MLS data. For an investor deploying capital in residential or commercial markets, that lead time is the difference between buying into appreciation and chasing it.

Transaction Velocity and Due Diligence

Beyond valuation, AI is compressing the transaction cycle in ways that matter for both buyers and sellers. Due diligence on commercial real estate typically involves months of document review — leases, environmental reports, title searches, zoning history, building inspection records. AI document review tools are reducing this review time by 60-70% without sacrificing accuracy, with the additional benefit of consistency: an AI system reviews every document with the same level of attention, rather than varying quality depending on which associate is working late on which day.

Contract drafting and negotiation support is similarly being compressed. AI tools trained on large bodies of real estate transaction documents can generate first-draft purchase agreements, flag non-standard clauses, and identify negotiating positions that have historically been accepted or rejected by similar counterparties. For high-volume transaction teams — brokerages processing dozens of deals monthly — these capabilities compound into significant competitive advantage.

The Risk Landscape

The flip side of AI-accelerated property pricing is AI-accelerated mispricing. In markets with thin transaction data — rural areas, specialty asset classes, highly unique properties — model confidence intervals widen dramatically. The risk of overconfident AI valuations being used to justify financing decisions or investment theses is real, and the regulatory framework for automated valuation models in lending contexts is still developing.

The practitioners getting this right treat AI valuations as a strong prior, not a definitive answer. They're using models to generate a confident starting point and a set of risk flags, then applying expert judgment to the exceptions. The institutions that will struggle are those that treat model output as ground truth in contexts where the training data is too thin to support that confidence.