|

AI document processing is reshaping corporate lending, KYC, and regulatory reporting — turning thousands of staff-hours into a competitive advantage. This article quantifies the cost savings, error reductions, and payback periods that large banks are actually realising after deploying intelligent document workflows at scale. |

The Hidden Cost Sitting in Your Loan Files

Walk into any corporate lending department and you will find the same scene: stacks of PDFs, spreadsheets cross-referencing PDFs, and analysts manually keying data between systems. It has always been this way. The question every CFO and COO should now be asking is how long it can stay this way — because the cost of standing still is no longer invisible.

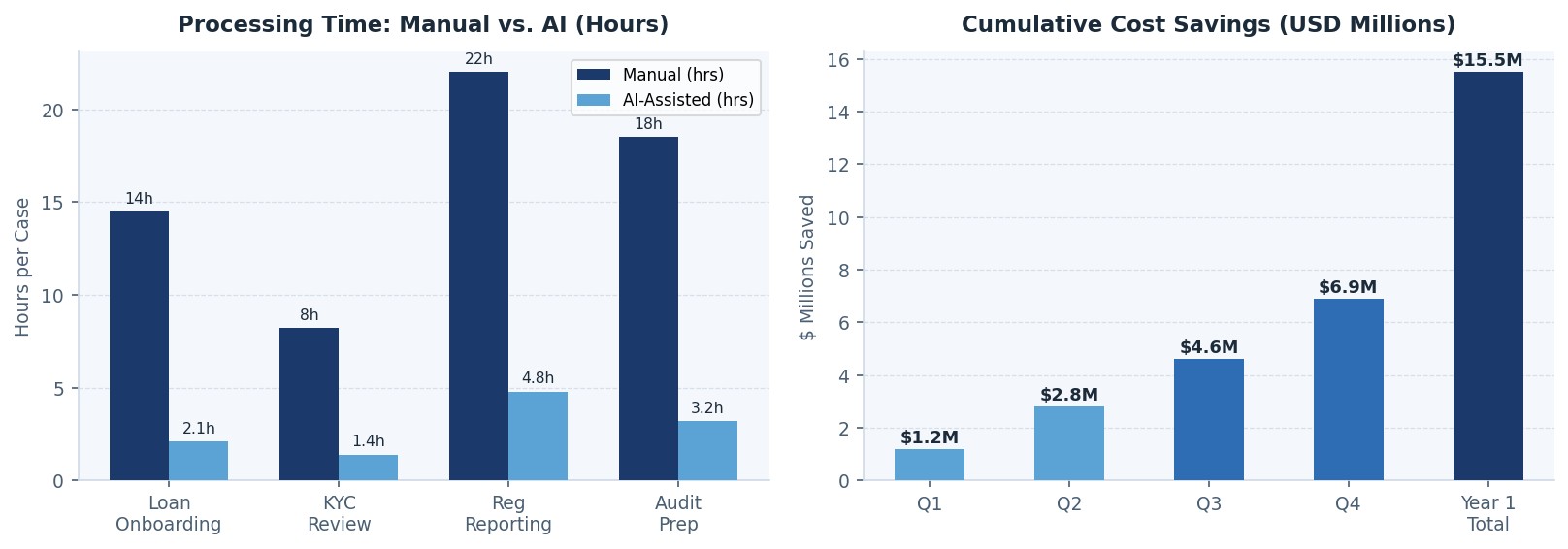

At one of the top five U.S. commercial banks, the document operations team calculated that their lending analysts spent an average of 14.5 hours processing a single loan onboarding package. KYC reviews consumed another 8.2 hours per counterparty. Regulatory reporting preparation averaged 22 hours per filing cycle. These are not outliers — they are industry norms.

When that institution deployed an AI-driven intelligent document processing (IDP) platform across those three workflows, the results landed well ahead of projections. Loan onboarding dropped to 2.1 hours. KYC to 1.4 hours. Regulatory reporting fell to 4.8 hours per cycle. The error rate on data extraction — previously running at 4–6 percent for complex multi-page credit agreements — declined to below 0.4 percent in production.

Where the Dollars Actually Come From

Executives who have been through software transformation cycles are right to push back on hours-saved projections. Hours saved do not automatically translate to dollars saved. What matters is how those hours get redeployed — and what the error reduction does to downstream rework and compliance exposure.

In the lending context, the financial case rests on three levers. First, capacity reallocation: analysts freed from document processing can handle a meaningfully larger pipeline without additional headcount. At a $2 billion commercial loan book, even a 20 percent improvement in origination throughput has seven-figure revenue implications. Second, rework elimination: a document error in a credit file does not stay in that file — it propagates into covenants, RAROC models, and regulatory submissions. Fixing it is expensive. Third, regulatory risk reduction: a missed field in a regulatory report can trigger examination findings that cost multiples of the underlying processing savings.

Modelling these three levers together, a mid-sized commercial bank with roughly $10–15 billion in assets should expect annualised savings in the range of $12–18 million from a comprehensive IDP deployment, with a payback period of 14–18 months on a program that typically costs $3–5 million to implement. The cumulative savings trajectory is steep: modest in the first quarter as the system trains on production documents, then accelerating sharply in quarters two through four.

What the Build-vs-Buy Debate Actually Comes Down To

Figure 1 — Processing Time (Manual vs. AI) & Cumulative Savings Across Four Key Document Workflows

The market for document AI in financial services has matured considerably. Purpose-built platforms with pre-trained models for loan agreements, ISDA schedules, prospectuses, and regulatory filings now exist at enterprise scale. The build-vs-buy question is less about capability and more about compliance architecture — specifically, where the data lives and how the model is retrained on proprietary document sets.

Banks that have tried general-purpose large language model APIs for document extraction have encountered predictable challenges: hallucinated field values on complex schedules, inconsistent handling of non-standard document formats, and audit trails that do not satisfy examiner standards. The leaders in this space are not running raw foundation models against their document corpus — they are running fine-tuned, domain-specific models within their own cloud perimeters, with every extraction decision logged and explainable.

The practical implication for technology and operations leaders: the ROI case for IDP in financial services is no longer speculative. The benchmarks exist. The reference architectures exist. What differentiates the programs that succeed from those that stall is not the technology — it is whether the business and compliance teams treat document AI as a core operations investment rather than an IT project.

Making the Business Case Stick

Presenting this ROI to a CFO or board requires anchoring the projection in production data, not vendor claims. The most credible approach is a structured pilot that runs AI extraction in parallel with manual processing for 90 days across a representative document sample — covering the full range of complexity, from standard term loan agreements to multi-tranche cross-border facilities. Measure extraction accuracy, exceptions requiring human review, and cycle time. That data becomes the foundation of the business case.

One regional bank that took this approach found that AI performed at or above human accuracy on 91 percent of documents in the pilot population, with human review queues concentrated in a predictable subset of non-standard structures. That 91 percent automation rate, applied to their actual document volumes, translated to a Year 1 savings figure precise enough to withstand internal scrutiny — and sufficient to clear their internal hurdle rate comfortably.

The era of treating document operations as a fixed, unavoidable cost in corporate banking is over. The firms that moved early on document AI are already compounding the advantage in pipeline velocity, compliance posture, and analyst retention. The gap between early movers and the rest of the market will widen with every credit cycle.

Comments (0)

Join the conversation!